Eighteen years ago, the Enron Corporation filed for bankruptcy following one of the largest corporate scandals in American history. Among its devastating effects, Enron’s collapse left nearly 5,000 company employees without jobs, precipitated the dissolution of Arthur Andersen LLP (one of the five largest auditing and accounting companies in the world), and left a lasting impact on the financial and legal world.

Featured Databases

Don’t miss out! Make sure you have the databases featured in this post. Follow the links below to start a trial today.

1. U.S. Congressional Documents

Featuring the complete Congressional Record Bound version, as well as the daily version back to 1980. This database also includes the three predecessor titles: Annals of Congress (1789-1824), Register of Debates (1824-1837), and Congressional Globe (1833-1873), as well as other important congressional material such as hearings, CRS Reports, and much more.

2. U.S. Federal Legislative History Library

In addition to the inclusion of comprehensive federal legislative histories published by the U.S. GPO and private publishers, this library also includes a unique finding aid based on Nancy Johnson’s award-winning work, Sources of Compiled Legislative Histories.

3. U.S. Presidential Library

This library includes such titles as Messages and Papers of the Presidents, Public Papers of the Presidents, CFR Title 3 (Presidents), Daily and Weekly Compilation of Presidential Documents, and other documents related to U.S. presidents.

4. U.S. Supreme Court Library

Complete coverage of the official U.S. Reports bound volumes as well as preliminary prints, slip opinions, and books and periodicals related to the U.S. Supreme Court are included in this library.

A Wall Street Treasure Plummets into Global Disgrace

A Company on the Rise

In 1985, Houston Natural Gas Company entered into a merger with Omaha-based InterNorth Incorporated, rebranding as Enron Corporation. Headed by Missouri-born founder and CEO Kenneth Lay, the natural oil and gas company hoped to become the premier natural-gas pipeline in America. After Congress approved legislation to deregulate the sale of natural gas, the Enron Corporation was able to sell energy at higher prices and become the largest seller of natural gas in North America by the early 1990s.

In 1990, the company hired Jeffrey Skilling to become CEO of Enron’s “Gas Bank”; Skilling, in turn, hired Andrew Fastow as an account director. Under their influence, Enron transitioned into a mark-to-market accounting method. Instead of measuring assets by their “actual” cost, mark-to-market accounting measures them by “fair value,” allowing Enron to log projected (instead of actual) profits.

In the latter half of the ’90s, innovations in the industry—including the company’s 1999 creation of EnronOnline—led the energy giant to become recognized as “America’s Most Innovative Company” by Fortune for six years in a row. By 2000, Enron’s stock sat between $80 and $90 per share.

Multiple Scandals Brewing

A Wall Street Journal article in September of 2000 explored the rise of mark-to-market accounting in the energy industry. Within its discussion, the article expressed concern about the strategy, and particularly the unknowns of how exactly a company has determined its earnings. Though the article was only published in the Texas regional edition of the Journal, several readers began to question how Enron made its money. Upon closer look, the company’s 10-K report revealed unusual transactions, significant debt, and erratic cash flow. Enron’s financials were increasingly complex, bewildering even to the company’s shareholders and analysts.

Meanwhile, the company began to face other concerns, including logistical difficulties, significant project losses, and operational challenges. Early in 2001, CEO Kenneth Lay resigned, leaving the position to his previous hire, Jeffrey Skilling. When stock prices plummeted that February, Lay sold portions of his Enron stock while assuring employees and investors to buy more shares. Andrew Fastow (promoted to CFO in 1998) worked with others to develop an elaborate scheme meant to hide the company’s growing mountains of debt—the transferring of stock into off-balance-sheet special purpose entities (SPEs). These practices helped maintain the image of a financially sound company when in reality, many of Enron’s subsidiaries were failing.

Though the company was instituting poor (and at times, illegal) accounting practices, its accounting firm Arthur Andersen LLP—one of the largest accounting firms in the world with a reputation for high standards—continued to sign off on its reports as it had for years.

The Reality of Enron Revealed

The investment community became increasingly skeptical about Enron as analysts began to dig deeper into the giant’s finances. At the same time, employees began to feel that accounting scandals may be imminent. In the fall of 2001, the Securities and Exchange Commission (SEC) began investigating the transactions between Enron and its SPEs. Within the next year, additional investigations by other federal and independent government agencies had been initiated, ultimately leading to criminal trials and convictions of the major executives involved. View the timeline below for an overview of the Enron Corporation’s downfall.

- October 2001:

- The SEC initiates its investigation into the Enron Corporation.

- Andrew Fastow is fired from his position as Enron’s CFO.

- Enron appoints its own Special Committee to investigate Enron’s transactions, headed by William C. Powers, Jr.

- December 2001:

- Enron and 13 of its subsidiaries file for bankruptcy.

- The SEC announces a subpoena against Andrew Fastow for testimony. Fastow chooses not to appear.

- January 2002:

- The U.S. Department of Justice confirms a formal Enron-related criminal investigation.

- Arthur Andersen LLP notifies the SEC, the FBI, and several congressional committees that a significant number of electronic and paper documents relating to Enron were destroyed.

- Enron fires Arthur Andersen LLP.

- February 2002:

- The U.S. General Accounting Office releases a report on Enron and its private pension plan.

- March 2002:

- President George W. Bush proposes a “Ten-Point Plan” for the improvement of corporate responsibility.

- The House Committee on Ways and Means approves H.R. 3669, a bill affecting employer stock in 401(k) retirement plans.

- April 2002:

- David Duncan, prior auditor for Arthur Andersen LLP, pleads guilty to an obstruction of justice charge and agrees to serve as a witness.

- The House passes H.R. 3763, regarding financial accounting oversight. The bill would ultimately become the Sarbanes-Oxley Act of 2002.

- June 2002:

- Arthur Andersen LLP is found guilty of obstruction of justice, ending the firm’s practice as an auditor.

- July 2002:

- President Bush gives a speech before corporate executives regarding corporate accountability and fraud.

- August 2002:

- Enron Executive Michael J. Kopper pleads guilty to conspiracy to commit wire fraud and conspiracy to engage in unlawful monetary transactions.

- October 2002:

- A 78-count indictment is brought against Andrew Fastow, including the charges of wire fraud, conspiracy to commit wire fraud, conspiracy to commit wire and securities fraud, money laundering, money laundering conspiracy, and obstruction of justice.

- January 2004:

- Andrew Fastow and his wife plead guilty—Fastow is sentenced to ten years in prison while his wife is sentenced to one year.

- Jeffrey Skilling is named in a 35-count indictment, to which he pleads not guilty. Charges include wire fraud, securities fraud, insider trading, and conspiracy.

- Founder Kenneth Lay is indicted on 11 criminal counts of fraud and misleading statements, to which he pleads not guilty.

- June 2004:

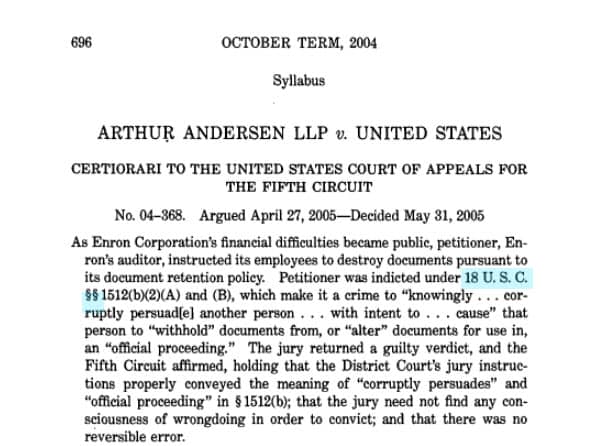

- Arthur Andersen LLP’s conviction is confirmed by the United States Court of Appeals, Fifth Circuit. Arthur Andersen appeals to the Supreme Court.

- May 2005:

- The Supreme Court takes on the Arthur Andersen case, unanimously overturning the firm’s previous conviction of obstruction of justice. Regardless, the firm was unable to recover.

- January 2006:

- Founder Kenneth Lay and former CEO Jeffrey Skilling go to trial in Houston.

- May 2006:

- Both Lay and Skilling are convicted—Lay on all six counts of conspiracy and fraud, Skilling on 19 of 28 counts of conspiracy, fraud, false statements, and insider trading.

- July 2006:

- Kenneth Lay dies of a heart attack.

- October 2006:

- Jeffrey Skilling is sentenced to 24 years in prison.

Aftermath of the Scandal

As its multiple accounting frauds came to light, Enron’s stock plummeted to $0.26 a share by the end of 2001. With each stock drop, Enron employees watched the value of their 401(k) pensions disappear, as well. By the end of 2001, Enron had collapsed, obliterating more than 5,500 jobs, $2.1 billion in pension plans, and billions of investor dollars under its weight.

Some employees received large bonuses in their final days, while more than 20,000 of Enron’s former employees lost their pensions. However, in 2004, the same employees won $85 million from a settlement in a class action lawsuit on behalf of the employees. Each employee received about $3,100 each.

New regulations and legislation were pushed through as a result of the Enron scandal. Perhaps most notably, the Sarbanes-Oxley Act of 2002 revamped the requirements for U.S. public company boards, management, and public accounting firms, and also created some provisions for private companies. Among its main provisions, the act established the Public Company Accounting Oversight Board to regulate the activities of auditors and public accounting companies. View the legislative history of the act in HeinOnline’s U.S. Federal Legislative History Library.

Want to Learn More?

At HeinOnline, we love to research topics of all shapes and sizes. We share that love on our blog by using HeinOnline databases to research anything and everything under the sun.

Don’t miss out! Receive this quality content right to your inbox by clicking Subscribe at the top of this post.